Editor’s Note – This “Twilight Zone”—the transition period between the end of quantitative easing and the first rate hike by the Fed, as it tries to normalize its fiscal policy.

SUA Staff feel it is necessary to warn of the possibility that this could cause great volatility for any investor or pension fund holder and the value of the US dollar.

Bank of America: Markets Are in a ‘Twilight Zone’ and It’s Time to Hold More Cash and Gold

By Julie Verhage – Bloomberg Business

In a note sent out this morning, Bank of America Merrill Lynch has a warning for investors:

Investors remain trapped in “The Twilight Zone”, the transition period between the end of QE and the first rate hike by the Fed, the start of policy normalization… until:

(a) the US economy is unambiguously robust enough to allow the Fed to hike and;

(b) the Fed’s exit from zero rates is seen not to cause either a market or macro shock (as it infamously did in 1936-7), the investment backdrop will likely continue to be cursed by mediocre returns, volatile trading rotation, correlation breakdowns and flash crashes.

For this reason we continue to advocate higher than normal levels of cash, adding gold and owning volatility in mid 2015.

Given extremities of liquidity, profits, technological disruption, regulation, income inequality…potential for a cleansing drop in asset prices cannot be dismissed. Most likely catalysts: Consumer, Rates, A-shares, Speculation, High Yield.

The note also highlights two interesting disconnects in the markets:

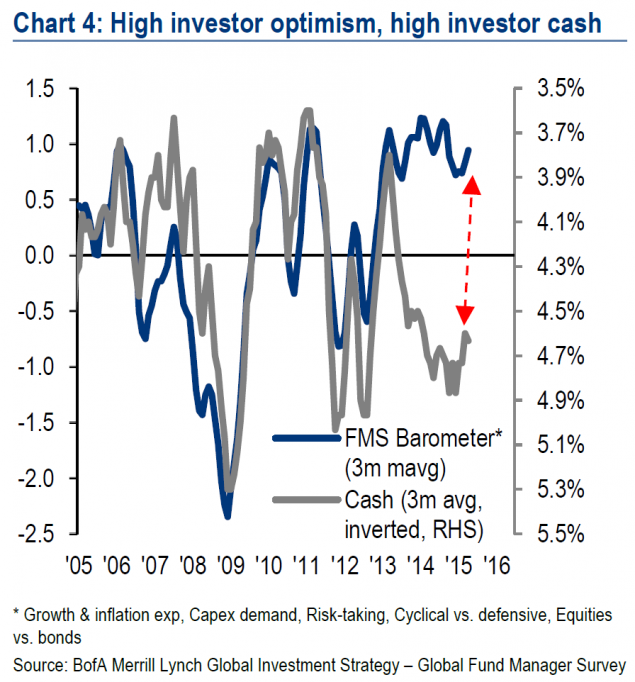

- Investors say they are optimistic, but there is a high level of cash on the sidelines;

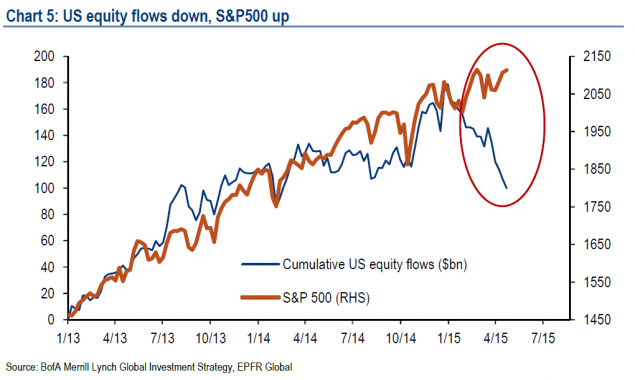

- U.S. stock prices are at record highs, but equity funds are seeing outflows;

Regarding the first point, one of Bank of America’s surveys showed investor sentiment as being “risk-on,” which it says is normally associated with less cash on the sidelines.

To the second point, the note says U.S. equity funds have suffered $100 billion of outflows in 2015 while the S&P 500 is near all-time highs, which its data says isn’t exactly typical.

The analysts led by Michael Hartnett attribute this to clients favoring European and Japanese equities at the expense of the U.S and that buying from those not captured in flow data (sovereign wealth funds, pension funds and central banks) could be what’s giving U.S. equity indices a boost.

The note hints that that you actually ought to sell in May and go away, at least for certain asset classes.

The summer months offer a lose-lose proposition for risk assets: either the macro improves and the Fed gets to hike, which will at least temporarily cause volatility; or more ominously for consensus positioning, the macro does not recover, in which case EPS downgrades drag risk-assets lower.

Edited by Suzanne M. Price – Staff Administration